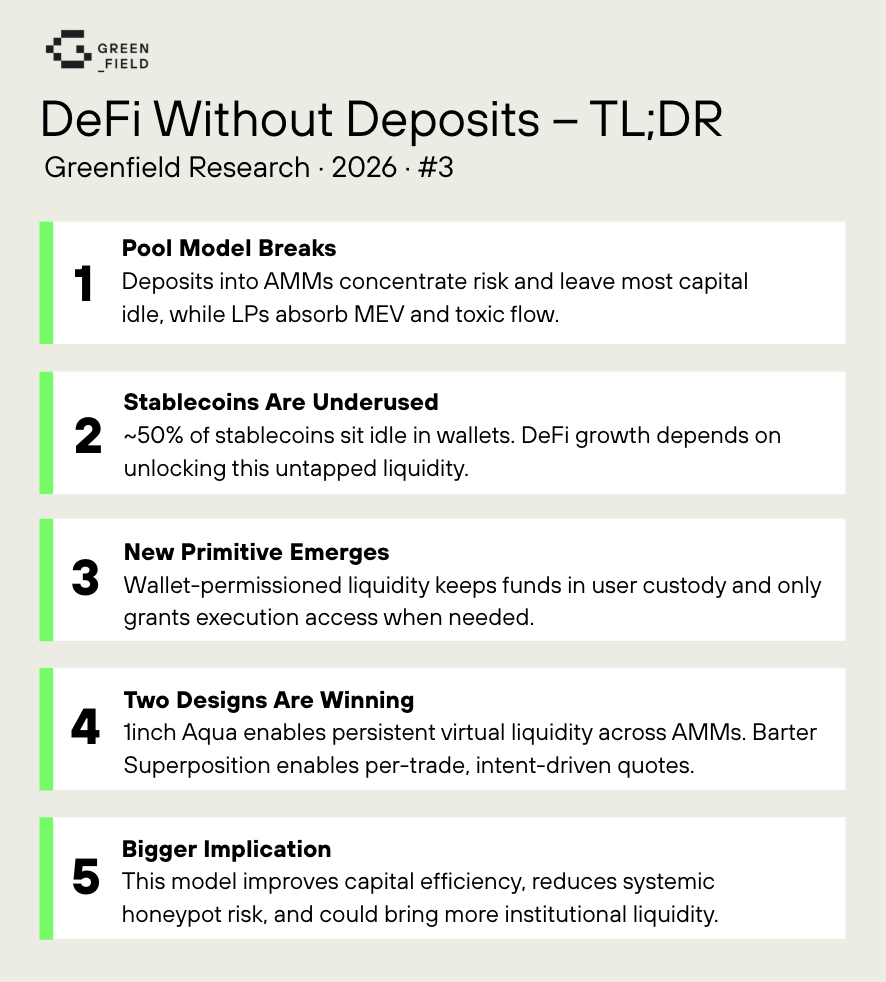

DeFi Without Deposits: Wallet-Permissioned Liquidity (Aqua & Superposition)

by Christoph Rosenmayr and Gleb Dudka – March 9, 2026

Special thanks to the 1inch (Aqua) and Barter (Superposition) team for feedback and review.

DeFi has historically required liquidity providers (LPs) to deposit assets into smart contracts to participate in liquidity provision and trading. This model enabled composability and atomic execution, but it also concentrated risk and led to structurally inefficient capital usage.

A new class of DeFi primitives is now emerging that flips this model: liquidity remains in user wallets and is permissioned for execution only when needed. Rather than owning liquidity, protocols orchestrate access to it.

This piece explores wallet-permissioned liquidity as an emerging DeFi design pattern, using 1inch Aqua and Barter Superposition as concrete case studies, and examines its implications for capital efficiency, risk, and adoption – including by more risk-aware and institutional capital.

Why pooled liquidity is less efficient

Since its inception, DeFi has been built around locking capital into pools where custody and ownership are delegated to smart contracts. These contracts coordinate access, allowing for deterministic atomic execution and composability across protocols.

However, pooled custody also concentrates risk. Large liquidity pools become honeypots, and failure is often catastrophic: exploits can drain all deposits in a single atomic transaction.

For AMMs specifically, passive LP pools lead to structurally inefficient capital usage. Liquidity is continuously available along the pricing curve, but only a small fraction is actually used for swaps. In practice, 84–95% of capital in top AMMs is idle in any given block, a problem that has worsened as liquidity has fragmented across fee tiers and competing AMM designs.

In addition, LP liquidity is offered unconditionally, regardless of market conditions or counterparty quality. This exposes LPs to MEV-related losses such as arbitrage-driven LVR. LPs could reuse the same capital across strategies and apply pre-trade filtering to avoid trading against toxic counterparties like arbitrageurs.

At the same time, wallet-based liquidity models improve the UX for end users. As Liquidity providers retain full access to their assets at all times, funds remain spendable directly from the wallet without withdrawal processes or claim steps, which transforms the user’s wallet into a true on-chain savings account.

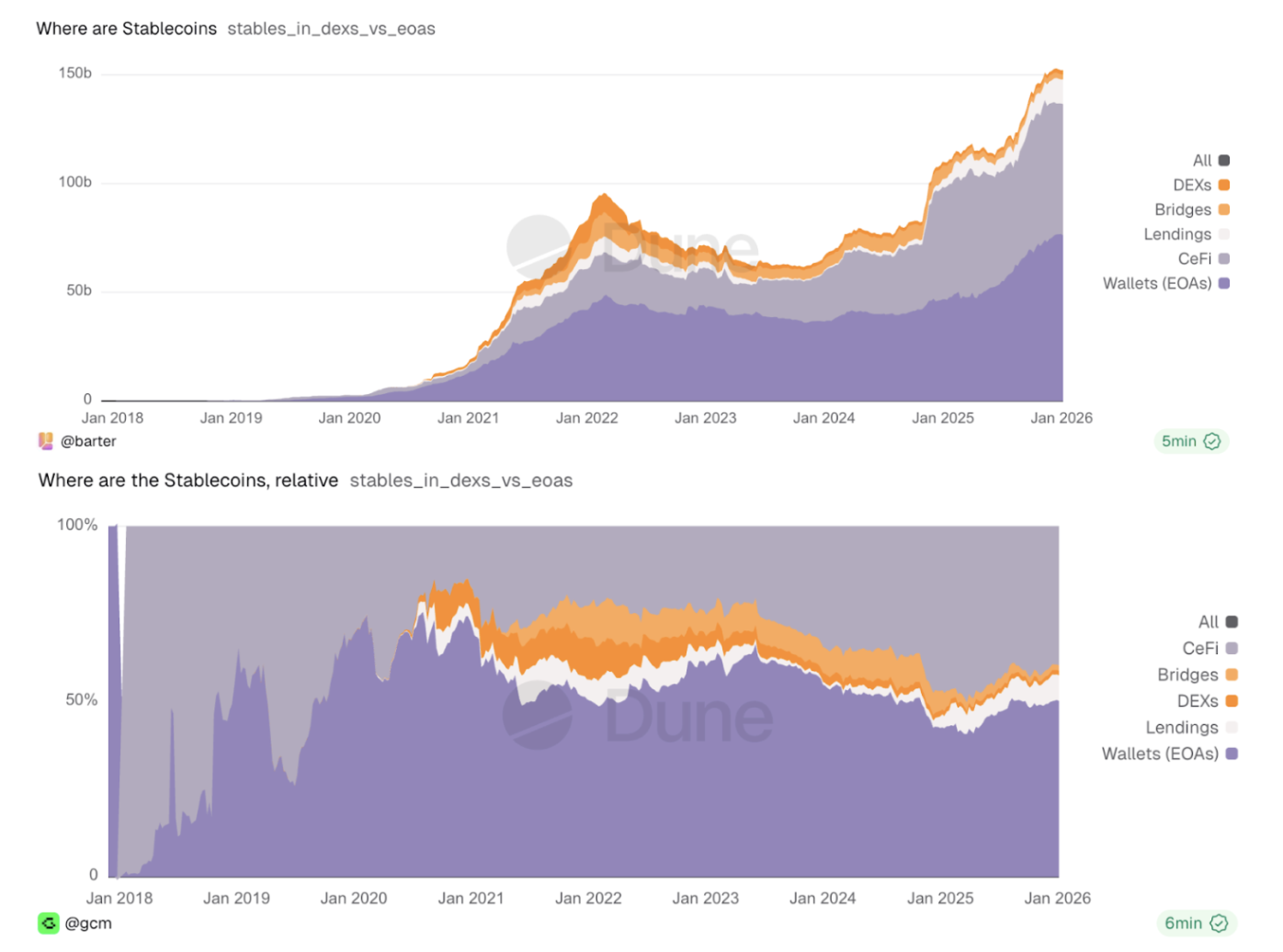

Where stablecoins reside | Source: dune

Stablecoins: the capital pool DeFi is missing

Despite continuous improvements to DeFi primitives and massive stablecoin growth, DeFi’s share of total stablecoin supply has remained flat or even declined over time.

Today, nearly 50% of stablecoin supply sits idle in EOAs (externally owned accounts = wallets), while roughly 40% resides in CeFi (centralized exchanges), a share that even steadily increased since early 2021.

While out of scope here, the decline of stablecoins in AMM LP positions underscores the structural issues described above. Even improvements like concentrated liquidity only marginally reduced idle capital (e.g., ~95% unutilized in Uniswap v2 vs ~84% in Uniswap v3). At the same time, more flow is being filled by prop-AMMs (e.g., on Solana) or intent/RFQ-based systems like CowSwap (a Greenfield investment).

For DeFi to grow, capturing even a small portion of idle stablecoins sitting in EOAs represents a large and relatively low-hanging opportunity. In contrast, stablecoins in CeFi are often already deployed productively (e.g., market making or lending) offchain but from an on-chain perspective, these are still also sitting idle and could also be used in wallet-permissioned liquidity models.

Hence, much of the capital parked in EOAs is there intentionally – due to risk preferences, treasury mandates, or regulatory constraints. But even capturing single-digit percentages of this pool would meaningfully expand DeFi’s addressable market.

Wallet-permissioned liquidity: a new primitive

We are now seeing new DeFi primitives built around explicit wallet permissions, allowing protocols to access liquidity directly from EOAs only at execution time, without requiring users to lock funds into smart contracts upfront.

In this model:

- Users retain custody of assets

- Protocols do not own liquidity

- Access is mediated via approvals and execution constraints

Importantly, wallet-permissioned liquidity is not about extracting yield at all costs. It is about enabling controlled, revocable participation in on-chain liquidity under clearly defined execution constraints, a different operational and custody model than traditional deposit-based yield strategies. LPs still bear pricing and inventory risks associated with their chosen strategies, but capital remains fully transferable and unencumbered in user wallets.

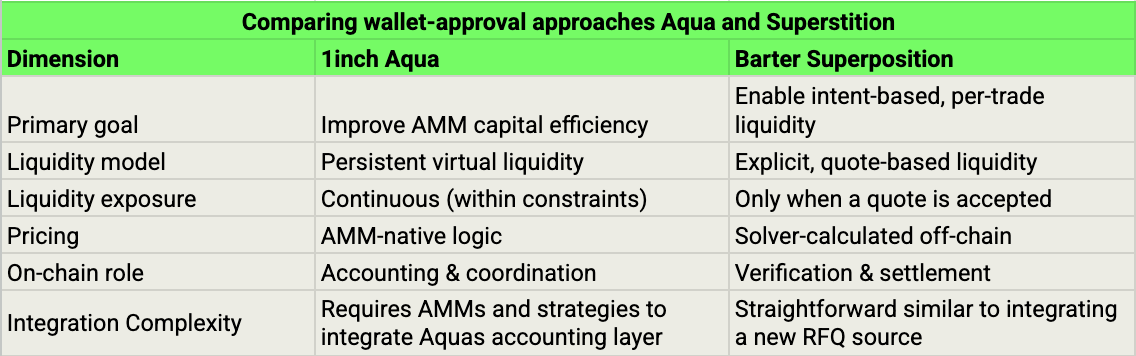

The two most prominent implementations today are Aqua by 1inch (a Greenfield investment) and Superposition by Barter. Both rely on ERC-20 approvals as a core design principle, but pursue fundamentally different goals.

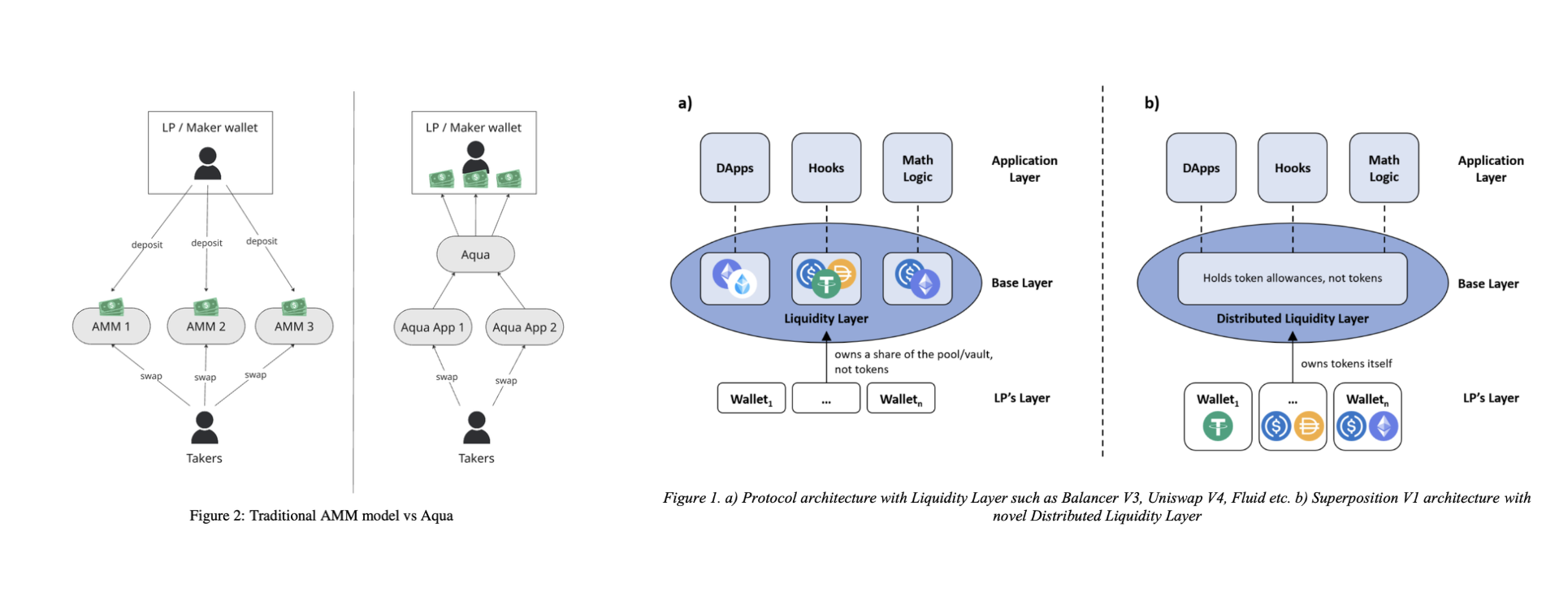

1inch Aqua Architecture & Barter Superposition Architecture, source: Aqua whitepaper & Superposition whitepaper

Aqua: virtual balances and persistent strategies

Aqua primarily addresses the underutilization of capital in AMMs. Users grant long-lived approvals to strategies, enabling liquidity to remain continuously available within defined constraints.

Aqua introduces SwapVM, an accounting layer that exposes virtual balances on-chain. Strategy developers can permissionlessly build strategies that read from these balances without requiring pre-funded pools.

For example, a single virtual balance can back multiple AMM instances (e.g., different fee tiers for the same pair). Liquidity is pulled directly from user wallets just-in-time when a trade executes, using each AMM’s native pricing logic.

SwapVM prevents overdraws and coordinates concurrent access across strategies, enabling the same capital to back multiple positions simultaneously and significantly improving capital efficiency. AMMs integrating Aqua reference virtual balances instead of on-chain token balances.

Superposition: explicit, intent-driven liquidity

Barter takes a different approach. Liquidity is not persistently available, but explicitly offered on a per-trade basis.

ERC-20 approvals define upper bounds, while execution authority is granted through off-chain signed quotes specifying price and size. These quotes are verified on-chain at settlement.

Liquidity is extended in response to swap intents (e.g., from CowSwap) or even other traditional DEX aggregators, with pricing computed off-chain by Barter’s solver infrastructure and validated via oracle checks.

In this model, no persistent liquidity state is exposed on-chain. Pricing and discovery happen off-chain, and on-chain contracts focus on verification and settlement.

The core goal is to make liquidity provision more profitable relative to traditional AMMs by allowing users to generate yield by filling profitable order flow while keeping assets in their wallets.

Considerations and risks

Approval-based DeFi still introduces risks, particularly around compromised or upgradeable spender contracts. However, the worst-case failure mode changes: attackers must execute individual transfers per wallet, rather than draining a pooled contract atomically. This is slower, more observable, and more amenable to circuit breakers.

Historically, many approval-based exploits stemmed from overly broad or lingering approvals rather than novel bugs.

That said, new challenges emerge:

- UX around monitoring and managing approvals

- Correct representation of virtual balances (Aqua)

- Principal–agent problems between users and solvers (Barter).

Liquidity discoverability is another key challenge. Without on-chain pools exposing balances, off-chain coordination or internal accounting layers are required. Integration is non-trivial, which explains why both 1inch and Barter benefit from already controlling significant order flow via their aggregator and solver infrastructure.

Finally, reliance on off-chain components introduces liveness, fairness, and censorship-resistance considerations.

Opportunities and implications

Over time, these primitives could be integrated directly into wallet UX, allowing users to deploy capital dynamically based on APY, volatility, or utilization – without moving funds out of custody.

This would further elevate the role of strategy managers and solvers as critical coordination layers. We may also see innovation in spot and perpetual orderbook designs, capital reuse across markets, and more sophisticated pre-trade filtering to avoid toxic flow.

However, primitives requiring withdrawal queues or delayed exits may struggle in this paradigm, as approvals can be revoked instantly.

Summary

We believe wallet-permissioned liquidity represents one of the most important emerging design patterns in DeFi.

By decoupling liquidity provision from custody, it has the potential to:

- materially improve capital efficiency and reduce cost of capital

- reduce systemic risk from pooled honeypots

- unlock participation from currently idle wallet-held capital.

If successful, these primitives could meaningfully expand DeFi’s addressable market and bring it closer to the needs of more risk-aware and institutional participants.

If you are building with wallet approvals or thinking about new liquidity primitives, reach out on email (christoph@greenfieldcapital.com) or on telegram (https://telegram.me/@thirdeye33) – this design space is just getting started.