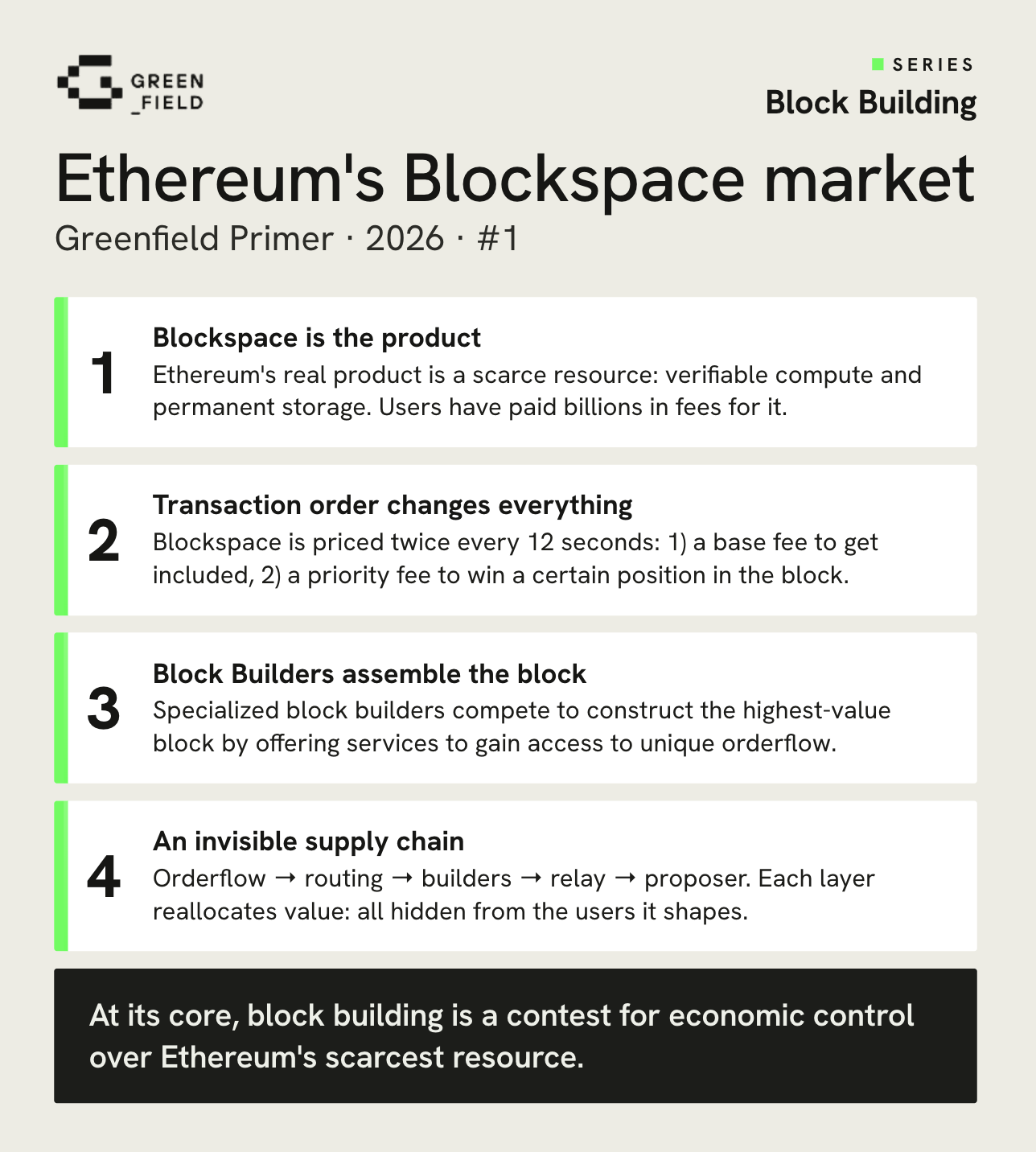

New Series: How Ethereum block building works today and why it matters

by Christoph Rosenmayr & Jascha Samadi – July 1, 2026

This is a high-level explainer of the Ethereum transaction supply chain and market structure. It aims to set the stage for readers unfamiliar with these topics, before we use deep on-chain data to quantify the transaction supply chain and its key players in our forthcoming “Block Building” research series. See also the thematically structured glossary below.

Blockspace is the scarce resource – the combination of verifiable compute and data storage secured by decentralized consensus. Ethereum’s core product is blockspace, and its main business is selling access to it. Blockspace consumers pay to have their transactions executed and permanently recorded on-chain. Historically, billions of dollars have been paid in fees to access this resource.

Every 12 seconds, a new Ethereum block is produced, raising the question of which limited set of transactions to include in this block and, often even more importantly, in which order these transactions are executed. This matters greatly because the ordering of events changes outcomes, as blockchains consist of sequential state changes in a database. If one swap executes before another, the second user may face a radically different and worse price than expected.

Before The Merge (Sep 2022), Ethereum miners ran simple algorithms to order transactions in their blocks. As DeFi applications grew in sophistication, however, the complexity of optimal transaction ordering increased dramatically. Post-Merge, these miners became validators, but the same underlying challenge remained. To keep validators lightweight and prevent $ETH stake from concentrating in the hands of whichever party had the most sophisticated block-construction capability, specialized block builders emerged as a separate role. They took on the complex work of assembling blocks so that validators could simply propose and attest.

One chain, many demands

The quality of blockspace is the primary differentiator between blockchains. But quality means something different depending on who you are — and this has given rise to a complex Ethereum supply chain aimed at improving how blockspace is allocated and better satisfying the distinct demands of each type of consumer.

This supply chain increasingly shapes the outcomes that matter most to every key stakeholder in Ethereum:

- Validators care about fees, the only non-dilutive revenue stream available to them.

- Retail users feel the effects most directly: the supply chain determines whether they suffer slippage, whether sensitive information is leaked from their transactions, and whether their transaction lands on-chain at all.

- Institutions represent a new and growing class of users coming on-chain, with unique demands around execution quality, privacy, and compliance that the supply chain is increasingly being built to accommodate.

- dApps & orderflow providers such as wallets, frontends, and applications rely on the supply chain both as a venue for innovation (via application-specific ordering) and as a monetization layer for the orderflow they generate.

Yet for all its complexity, this supply chain is largely invisible to users. Most people transacting on Ethereum have little to no awareness of the infrastructure shaping their experience.

The easiest way to understand this market is to break it into layers: where transactions come from, how they are routed, how builders compete for them, and how the winning block is finalized.

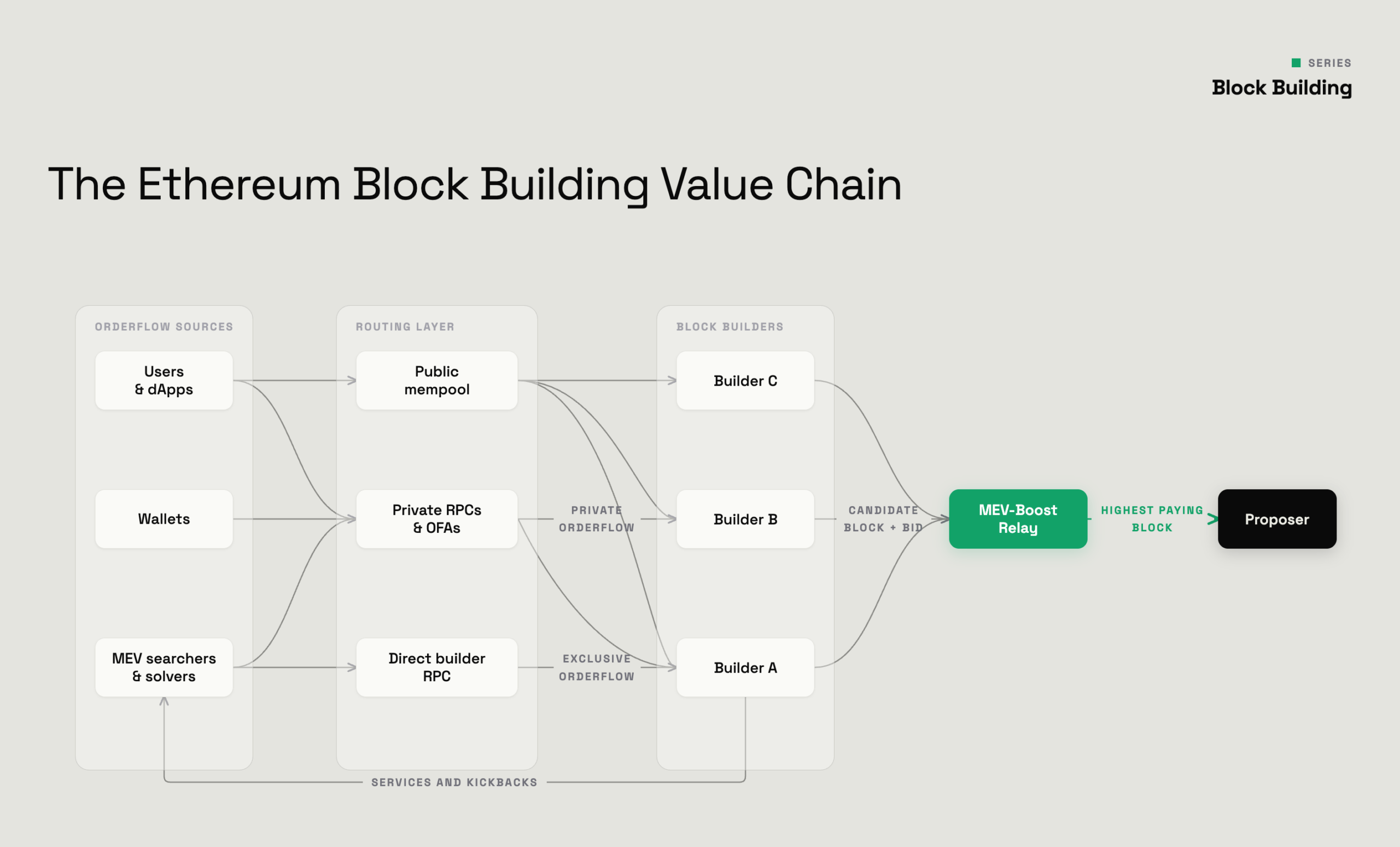

The Orderflow Layer

Orderflow is the set of all transactions looking to be included on-chain. This includes users and wallets routing swaps or transfers, dApps sending batched or application-generated transactions, solvers competing to execute user intents, or MEV searchers aiming to capture profitable trading opportunities.

However, not all orderflow is equally valuable as blockspace is priced on two very different dimensions:

- The inclusion market: This determines whether a transaction gets into the block at all. If the network is congested, inclusion becomes more expensive and vice versa. This is priced via the base fee for compute (burned in EIP-1559) and is the part most users are familiar with.

- The position market: As mentioned in blockchains, transaction order changes outcomes. If a sandwich bot trades before you, you get massively worse slippage. If one arbitrageur trades first, the opportunity disappears. That means the same transaction can be very valuable in one position and worthless in another position later in the block. This is where the majority of the orderflow value comes from, as some transactions are competing not just for inclusion, but for access to a specific state before it changes. A rational arbitrageur should be willing to pay up to almost the entire profit he can capture in order to guarantee he actually executes the trade first. This fee is often paid via priority fees. In comparison, for a simple USDC transfer, the exact position in the block matters little and should therefore not pay any meaningful priority fees.

That is also how and why MEV exists. It emerges because priority access to a shared state always has economic value. In traditional finance and orderbook, this priority access also has value, but via first-come, first-served is priced via investments in latency improvements rather than priority fees and block values.

The Routing Layer

Once orderflow providers create transactions, the routing layer determines which parties see this transaction before inclusion. In the simplest model, a transaction is broadcast to the public mempool, where anyone can observe it. This creates risks as public transactions can be copied, backrun, or sandwiched by actors observing the public mempool. These risks have led to a growing share of orderflow preferring more private channels, such as private PRCs/OFAs (Orderflow Auctions), which reduce information leakage, thereby improving execution and returning part of the extracted value to orderflow providers.

Some order flow goes even further and is sent directly to the block builder via direct integrations of builder RPC. This is most common for sophisticated flows that care most about even more granular ordering constraints, conditional execution, latency or kickbacks when overpaying for block position, which are services only block builders can offer.

The Block Builder Layer

Once order flow reaches the block builders, raw transactions have often been significantly enriched by being bundled or having conditional logic applied by others in the supply chain. The builder’s job is now straightforward in theory: to assemble the most valuable block from all transactions and their associated fees to maximize the total value that can be paid to the proposer.

This relies on sophisticated algorithms and latency-efficient infrastructure to simulate thousands of candidate blocks per slot to find the order of transactions that produces the highest valued final block.

However, block builders don’t start with a shared input of transactions, as access to order flow received from the routing layer is uneven. A builder only seeing transactions from the public mempool will never be able to build a more valuable block than a builder also receiving unique orderflow directly.

This makes block builders service providers to orderflow providers and forces them to innovate and improve their offering to attract and retain high-value orderflow providers.

Finalizing the block

During block construction, builders submit their highest valued blocks and bids to the relay. The relay acts as the intermediary to prevent validators from stealing the block or builders from submitting invalid blocks by simulating blocks.

When submitting bids to the relay, a builder does not need to bid the full value of its block, but rather only outbid the next-best rival in the auction. The spread between the true value of its block and the winning bid is where builder profit comes from. This is why unique orderflow sources are so important to builders: transactions seen by every builder are quickly competed away in the auction, while differentiated orderflow allows a builder to retain more of the value they create.

The validator chosen as proposer for the slot now just needs to select the highest-paying valid block offered through relays, which is then propagated to the network, and the ordered set of transactions becomes the next Ethereum block.

The Greenfield “Block Building” series

In our upcoming Research, we move from theory to data. Using on-chain data from 2024 through 2026, we map Ethereum’s priority fee landscape, identify the largest sources of valuable orderflow, and analyze how those relationships shape builder profits, competition, and market structure. To understand questions such as

- Which orderflow is actually driving block value?

- How much of the block value is now MEV-driven?

- Which builders are winning economically, not just by block count?

- How exclusively is high-value orderflow shared with select builders, and which builders are winning or losing new order flow providers?

- And how is all of this changing Ethereum’s market structure?

The answers to these questions will make one thing clear: block building is, at its core, a competition for economic control over Ethereum’s scarcest resource. The stakes are higher than most users realize.

Ethereum Transaction Supply Chain Glossary

Core Infrastructure

Validator: The post-Merge equivalent of a miner. Validators propose and attest to blocks on Ethereum, earning fees as their primary non-dilutive revenue stream. They are intentionally kept lightweight, delegating block construction to specialized builders.

Block Builder: A specialized party that constructs the most profitable block possible by ordering transactions, competing to have their block selected by a validator. Emerged as a distinct role after the Merge.

Relay: A trusted intermediary between block builders and validators. Relays receive blocks from builders, verify their validity and value, and pass the most profitable one to the validator, without the validator needing to trust the builder directly.

Proposer: The validator selected in a given slot to propose the next block to the network.

MEV & Transaction Ordering

MEV (Maximal Extractable Value): The maximum value that can be extracted from a block by reordering, inserting, or censoring transactions. Originally called “Miner Extractable Value” pre-Merge.

Bundle: An ordered array of transactions submitted by e.g. MEV-searchers, designed to be executed in a specific sequence. Builders incorporate bundles into blocks which capture MEV opportunities.

MEV-Searcher: A sophisticated actor that scans the mempool for MEV opportunities and submits transaction bundles to builders.

Mempool: The public waiting room for unconfirmed transactions. Transactions sit here before being included in a block.

Slippage: The difference between the expected price of a trade and the actual execution price, often caused by transaction ordering or market movement between submission and inclusion.

PBS & Architecture

PBS (Proposer-Builder Separation): The post-Merge architectural principle of separating the role of block construction (builder) from block proposal (validator/proposer).

MEV-Boost: The dominant middleware used today that implements PBS off-chain. Validators run MEV-Boost to receive blocks from a competitive market of builders via relays, maximizing their revenue.

Slot: The 12-second window in which a selected validator must propose a block. Each slot = one block opportunity.

EIP-1559: The Ethereum improvement proposal (implemented in August 2021) that restructured transaction fees into a base fee (burned by the protocol) and a priority fee (tip paid to the validator). It made fee estimation more predictable for users and introduced ETH as a deflationary asset, while also shaping how builders think about transaction inclusion.

Orderflow & Distribution

Orderflow: The stream of transactions generated by users, wallets, apps, and other frontends. Controlling or routing orderflow is increasingly valuable, as it determines who can extract MEV and who earns fees.

Orderflow Provider: Any party that generates or routes user transactions, including wallets, dApps, and frontends. These players increasingly monetize their orderflow by routing it to builders or private mempools.

OFA (Order Flow Auction): A mechanism where orderflow providers (wallets, apps) auction off their users’ transactions to searchers or builders. The winning bidder gets the right to include and potentially extract value from the transaction, with a portion of the proceeds returned to the user or the orderflow provider.

Private Mempool / Private Orderflow: Transactions submitted directly to builders, bypassing the public mempool. Protects users from front-running and gives builders an informational edge.

RPC (Remote Procedure Call): The interface through which wallets and users submit transactions to the network. Custom RPC endpoints (e.g. from MEV protection services) can route transactions privately, bypassing the public mempool to reduce front-running risk.

Application Layer

Application-Specific Ordering: Transaction ordering rules defined by a dApp itself, rather than left entirely to the builder. Allows protocols to enforce fairness, reduce MEV, or create custom execution environments.

Intent: A higher-level expression of what a user wants to achieve (e.g. “swap X for Y at best price”) rather than a specific transaction. Solvers compete to fulfill intents optimally, abstracting away execution complexity.

Solver: A party that competes to fulfill user intents, finding the optimal execution path across liquidity sources and submitting the resulting transaction(s) on the user’s behalf.